Everyone dreams of finding that one stock that can turn ₹1 lakh into ₹50 lakh. For a few investors, that dream came true. Some small-cap companies have quietly gone from being under-the-radar names to massive wealth creators over the last few years.

Their businesses changed, earnings took off, and those who held on saw outsized gains, without chasing trends or timing the market. But when a stock has already run up 50x, it's only natural to wonder-is it too late now? Can these companies continue to deliver, or has most of the upside already been realised?

Let’s take a look..

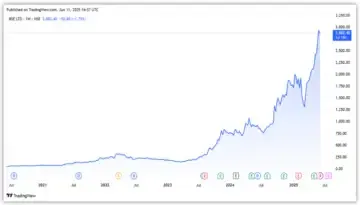

#1 Bombay Stock Exchange

Operating since 1875, theBombay Stock Exchange is Asia’s oldest and first stock exchange. It is also the world’s fastest, with a trading speed of 6 microseconds. It offers trading in equities, currencies, debt instruments, derivatives, and mutual funds.

Its mutual fund platform, BSE Star Mutual Fund, is India’s largest online mutual fund platform, processing over 2.7 million transactions monthly and adding around 0.2 million new Systematic Investment Plans (SIPs) each month.

BSE operates across three business segments: Trading and Clearing, Distribution, and Services to Corporates. In FY25, revenue almost doubled to ₹32 billion, up from ₹15.9 billion in FY24. Net profit surged 71% to ₹13.2 billion, with margins expanding 23 percentage points to 51% as operating leverage kicked in.

BSE is a Big Beneficiary of Derivatives Boom

BSE's revenue has seen strong growth from the derivatives segment. In FY25, equity derivatives contributed 44% (₹14.2 billion) to total revenue, up from just ₹1.8 billion in FY24. This growth was driven by a surge in average daily premium turnover, which rose from ₹71.6 billion in Q4FY24 to ₹118 billion in Q4FY25.

This came despite a 46% drop in average daily notional turnover during the second half of FY25. Regulatory changes in the Future and Options segment worked in BSE's favour, as non-closing trading activity increased, boosting premium turnover and lowering regulatory costs.

Equity transaction charges contributed another 9.4% (₹3.0 billion) of revenue. Overall transaction charges almost tripled to ₹20.3 billion in FY25, up from ₹7.1 billion in FY24.

Strong Performance Across Segments

BSE StAR MF’s revenue also grew, benefiting from structural growth, with revenue rising 80% to ₹2.3 billion. A 61% increase in the number of orders drove the growth. Revenue from services offered to corporates, such as annual listing fees, fees for corporate actions, and compliance filings, also increased by 40% to ₹4.9 billion.

Looking ahead, BSE's Asia Index plans to launch around 40 new indices across sectors in FY26 - double the number in FY25 - to tap the growing trend of passive investing. It also plans to improve the utilisation of the 100 additional server racks it recently added.

Valuation Running Ahead of Fundamentals

From a valuation standpoint, BSE trades at a price-to-equity multiple of 89x, well-above the 10-year median of 29x. Increased member participation, colocation monetization, and sustained momentum in premium turnover will be key growth drivers for BSE.

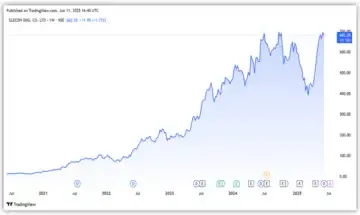

#2 Elecon Engineering

Elecon Engineering is among Asia’s largest providers of industrial gear solutions. According to ICRA, it holds a 38-40% market share in the domestic market, making it a leading player. The company is also a major name in material handling equipment (MHE).

Elecon benefits from its strong design and engineering expertise, which enables it to offer complex products. This is evident from its ability to secure orders for marine gear from the Indian Navy.

Strong Financial Performance

Elecon reported a strong overall performance in FY25. Revenue increased 15% from last year to ₹22.3 billion, in line with guidance. The gear division contributed 79% of total revenue, while MHE contributed 21%.

On a geographic basis, domestic revenue accounted for 77% of the total, with the remaining 23% coming from international markets. Elecon currently serves customers in over 95 countries.

While the gear segment grew modestly at 6%, the MHE business saw a sharp 73% rise in revenue to ₹4.6 billion. Domestically, revenue grew 16%, while international sales rose 13%. EBITDA stood at ₹5.4 billion, with a margin of 24.4%. Net profit rose 17% to ₹4.2 billion. EBITDA stands for earnings before interest, taxes, depreciation, and amortization.

Strong Demand Across Key Sectors

The robust growth was driven by strong demand both in India and abroad. Domestically, steel, power, and cement sectors saw increased activity, boosting order flow. The overseas market is also seeing solid momentum.

Elecon ended FY25 with an open order book of ₹9.5 billion, up from ₹7.9 billion a year ago. Its order intake increased 19% from last year to ₹24 billion in FY25. Enquiry levels remain robust across both gear and MHE segments. MHE is seeing steady demand from the steel, cement, and power industries.

The company aims to increase its global market revenue contribution from the current 23% to 50% of total revenue by FY30. From a valuation perspective, it trades at a P/E of 37x, well above the 10-year average of 21x.

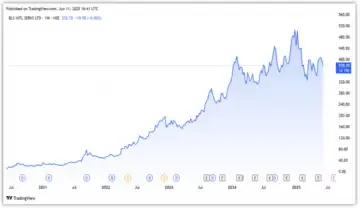

#3 BLS International Services

Established in 1983, BLS International is one of the largest providers of visa, passport, consular, and citizenship services, with a presence in over 70 countries.

It handles administrative and non-judicial processes for the visa application process, from initial submission to final approval.

Strong FY25 Performance Led by Both Core and Digital Segments

In FY25, BLS revenue rose 31% from last year to ₹21.9 billion, driven by both organic expansion and acquisitions. It operates under two business segments: visa and consular, and digital. The former contributed 75% of the revenue, and the latter 25%.

Visa and consular revenue remains the key revenue driver, rising 21% to ₹16.5 billion. A 31% rise in the number of applications to 3.7 million, along with a 35% increase in net revenue per application to ₹2,903, drove the growth. Segment EBITDA margin expanded 12.4 percentage points to 34.5%.

The digital business revenue grew by a massive 71% to ₹5.4 billion, driven by increased volume and transaction volume. However, margins were lower at 11%, down 3.3 percentage points.

Overall, EBITDA grew 82% to ₹6.3 billion, while margins expanded 8.1 percentage points to 20.6%. Cost optimization, transition from a partner-driven model to a self-managed model, and integration of new businesses led to margin expansion.

As a result, net profit rose 66% to ₹5.4 billion. BLS also has a strong balance sheet with a net cash position of ₹9.3 billion as of Q4FY25.

Looking ahead, the company has been actively pursuing acquisitions, deploying ₹10 billion in FY25 across various deals. Future revenue visibility remains strong, with multiple government contracts worth $1-2 billion up for renewal.

The company is a proxy for rising international travel demand. The BLS is expected to benefit from a steady increase in visa demand, driven by rising disposable incomes and government efforts to promote tourism.

In addition, easing of visa regulations and visa-free travel arrangements, such as the ASEAN visa, are also expected to support long-term growth. These factors together create a growth factor for sustained demand in the company’s Visa services.

Valuations in Line

Valuation-wise, the company trades at a P/E of 30, in line with the 10-year median of 32x.

Conclusion

All three businesses discussed above have delivered strong returns in the last five years. Operating leverage, network effects, and most importantly, the derivatives boom have led to a strong re-rating in the BSE stock price. In contrast, Elecon and BLS have benefited from the infrastructure and travel boom.

While structural tailwinds remain, BSE’s valuation remains stretched. On the other hand, Elecon is expensive, while BLS’s valuation offers relative comfort.

Disclaimer:

Note: Throughout this article, we have relied on data from https://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Contact to : xlf550402@gmail.com

Copyright © boyuanhulian 2020 - 2023. All Right Reserved.